Early vs. late retirement

Although most people expect to retire between age 60 and 65, there is in fact no preset age or time limit on retirement. It all depends on your situation, and you’re the only person who knows about that.

- Your health: Are you healthy? Starting to see health problems cropping up? You’ll need to be in shape if you want to embark on retirement projects like seeing the world or taking your pastimes to the next level. Your physical and mental health are just as important to your retirement as your financial health.

- Your motivation: Do you still derive some personal satisfaction from doing your job? Are you still motivated to go to work in the morning? In short, try to rate how happy you are in your professional life.

- Your social life: If most of your social life is connected to your job—sports, leisure, getting together with coworkers who are in fact your friends—think about whether that can continue after you retire. If not, will you miss it? A job is often a lot more than just a paycheque.

- Your personal situation: Then again, sometimes bad things happen so you have to retire earlier than you want to. Things like losing your job, caring for loved ones, or having health problems of your own. If that happens, there are a lot of things to consider that can help reduce the financial impact of premature retirement on your retirement plans.

What to weigh up before retiring early?

Government benefits

Most government pensions in Canada are available when you turn 65, but many can be taken early or delayed.

- In Quebec, the Québec Pension Plan, or QPP, provides a monthly pension to workers age 60 and over who meet the eligibility requirements. The equivalent of the QPP in the rest of the country is the Canada Pension Plan, or CPP. Although many people wait till they’re 65 to claim their pension, you can start collecting it when you’re 60, although you won’t get as much. You can also wait to claim your pension till you’re 70. The longer you wait, the bigger your lifetime annuity will be.

- There’s also Old Age Security, or OAS, from the Government of Canada. The minimum age for OAS is 65. There too, you can wait till you’re 70 and get more. If however you’re eligible for the Government of Canada’s Guaranteed Income Supplement, delaying your OAS isn’t such a good idea. The supplement doesn’t increase if you wait. You’re better off taking both at the same time increase your monthly income.

If for example you want to retire at age 55, you won’t get any government benefits till you turn 60 or 65. You’ll need to live off your personal savings, investments, and rental income from buildings if you own any as well as part-time work and your employer’s retirement plan.

Good to know: Even if you retire early, it’s a good idea not to claim your government pensions till you’re 70. That way, you’ll get more money you can set aside to give yourself an indexed life-long safety net. It’s an additional layer of protection, especially with life expectancy getting longer all the time. But if for instance your health is iffy, you might be better off collecting earlier and enjoying your life. Talk it over with your financial advisor.

Taxes

If you collect a pension while working full time, your income tax might go up. Take the time to look into how your pensions will affect your taxes. If you’re part of a couple, you might be eligible for income splitting.

Good to know: Collecting your pension and working full time doesn’t help. Things work out better financially if you’re working part time.

Your financial resources

Naturally you’ll need to figure out your resources before opting for early retirement.

- How’s your retirement plan coming along?

- Have you reached your goals?

- Are you getting close or do you need to pick up the pace and save as much as possible?

The biggest financial loss associated with retirement is your annual pay. That’s why you need to take an in-depth look at where you stand before retiring early. You’ll need a solid idea of how much money in savings you’ll need after you retire.

The last thing you want is to have to go back to work a few years later when you realize your savings weren’t enough. The younger you retire, the more you’ll need to rely on other sources of income.

Stay informed

Sign up for our newsletter to get recent publications, expert advice and invitations to upcoming events.

Phased or full retirement?

You can retire and quit working all at once, but you can also continue working part time or even gradually slow your pace—what’s known as phased or progressive retirement.

Up for phased retirement?

Phased retirement has its share of advantages, but it has its limits too.

Advantages:

- You might, for example go from a 5-day work week to 4 days.

- It lets you gently transition from workaday life to retired life. You can stretch it over a period of months or even years.

- It means you can stay active longer while maintaining that sense of accomplishment you experience at work.

- It gives you chance to gradually get used to making less money.

- If things don’t go quite the way you wanted them to financially, you can keep working a little longer.

- You can use your income from working part-time to pay into your RRSP—at least till age 71 when your RRSP matures. But you can pay into your spouse’s RRSP if he or she is under 71. You might also put the money into your TFSA or other savings account.

Considerations:

- The temptation to dip into your retirement savings to make up for your reduced job income (since you’re working fewer hours).

- A lack of motivation at work, since you won’t be there as often.

- You’ll be required to keep paying into the Québec Pension Plan (QPP) or Canada Pension Plan (CPP) as soon as you make more than the annual basic income exemption of $3,500. However, those contributions will increase your retirement income down the road. Outside Quebec, CPP contributions are optional when you turn 65.

- If you have a pension plan with your employer, find out how working less hours will affect your pension. Some pensions are based on your last 5 years of salary, for example, while others are based on your 5 best consecutive years. In the first case a phased retirement would end up reducing your monthly pension payment, while in the second case it wouldn’t have any impact.

If you’re in phased retirement, you should be able to claim your government pension later. If not, talk about it with your advisor.

Hankering to work part-time after you retire?

You could also retire and find a new part-time job for some extra income. Here too there are pros and cons.

Advantages:

- A part-time job can help you stay active and maintain a busy social life while keeping you sharp and in shape.

- You can adapt your work to your schedule.

- You can work in a different field than before, perhaps something connected to a hobby, pastime, or sport that you like.

- You’ll have a source of extra income in spite of your taxes.

- You can use your income from working part-time to pay into your RRSP—at least till age 71 when your RRSP matures. But you can pay into your spouse’s RRSP if he or she is under 71. You might also put the money into your TFSA or other savings account.

Considerations:

- The extra income might push you into a higher tax bracket.

- You’ll be required to keep paying into the Québec Pension Plan (QPP) or Canada Pension Plan (CPP) as soon as you make more than the annual basic income exemption of $3,500. However, those contributions will increase your retirement income down the road. Outside Quebec, CPP contributions are optional when you turn 65.

- Your Old Age Security benefit might be reduced or disappear if your net individual income goes over $80,000. People eligible for the Guaranteed Income Supplement can take a big tax hit from working part-time. Talk it over with your financial advisor.

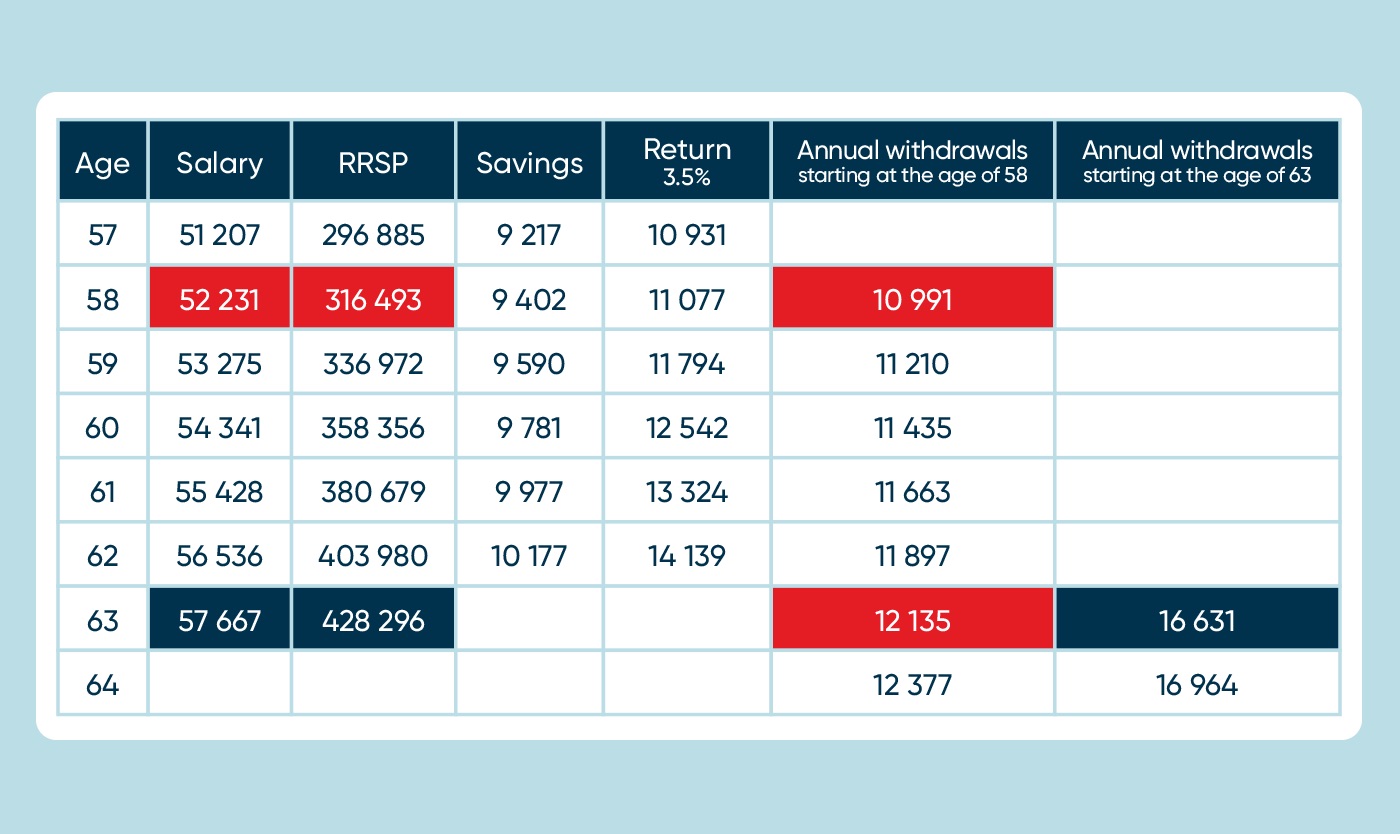

Fictional example of the financial effects of early retirement

To show you how it all works, let’s take a look at two imaginary 58-year-olds. They both have the same take-home pay and every year they put 18% of their salary into an RRSP that generates an average annual return of 3.5%. One retires at 58 while the other waits 5 years longer before tasting the joys of retirement at 63.

We've set a goal of their savings lasting until they're 95.

The person who retires at 58 retires making $52,231 a year and has $316,493 in an RRSP.

The person who retires at age 58 withdraws $10,991 in the first year. When that person turns 63, the amount, which is indexed, will be $12,135. Meanwhile, the person who retires at age 63 withdraws $16,631, or $4,496 more (not including the gain in salary during the additional 5 years).

In our example, the person retiring at age 63 had an additional $277,247 in gross earnings, and therefore was able to contribute an additional $111,803 to their RRSP, over 5 years. Actually the difference is even greater because the person who retired at age 58 has already started withdrawing from their RRSP. But there is more to life than money: the person who retired at 63 also had to go to work every morning for the last 5 years. Working sometimes comes with obligations and less free time.

The takeaway here is that if the financial side of early retirement is properly wrapped up, you’ll rest easy. All that’s left is to enjoy the new adventure that lies ahead. Get together with an advisor to talk things over and plan your retirement. You have questions. We’re here to help.