What’s a paycheck stub?

Alright, first off, if your pay stub reads “statement of earnings” instead, don’t worry, it’s the same thing. It’s something your employer is legally required to give you each time you get paid, either in hard copy or electronically.

Whether you’re paid weekly or biweekly (like most employees), whether your payday is Tuesday or Thursday, whether you’re a seasonal, temporary, or permanent worker, you’re supposed to receive a pay stub from your employer.

You may need your pay stubs for various purposes, such as applying for a loan. It’s also a good idea to use the last statement of each year to validate the figures on your income tax forms (T4 slips, etc.) and make sure no errors have been made.

Good to know: Pay stubs can also be used to check if your employer has made any mistakes, e.g., in your number of hours worked or your overtime hours, which are often paid at a higher rate. So make sure you have a look at them.

How to read your pay stub?

The first thing to know is that pay stubs are generally divided into four sections:

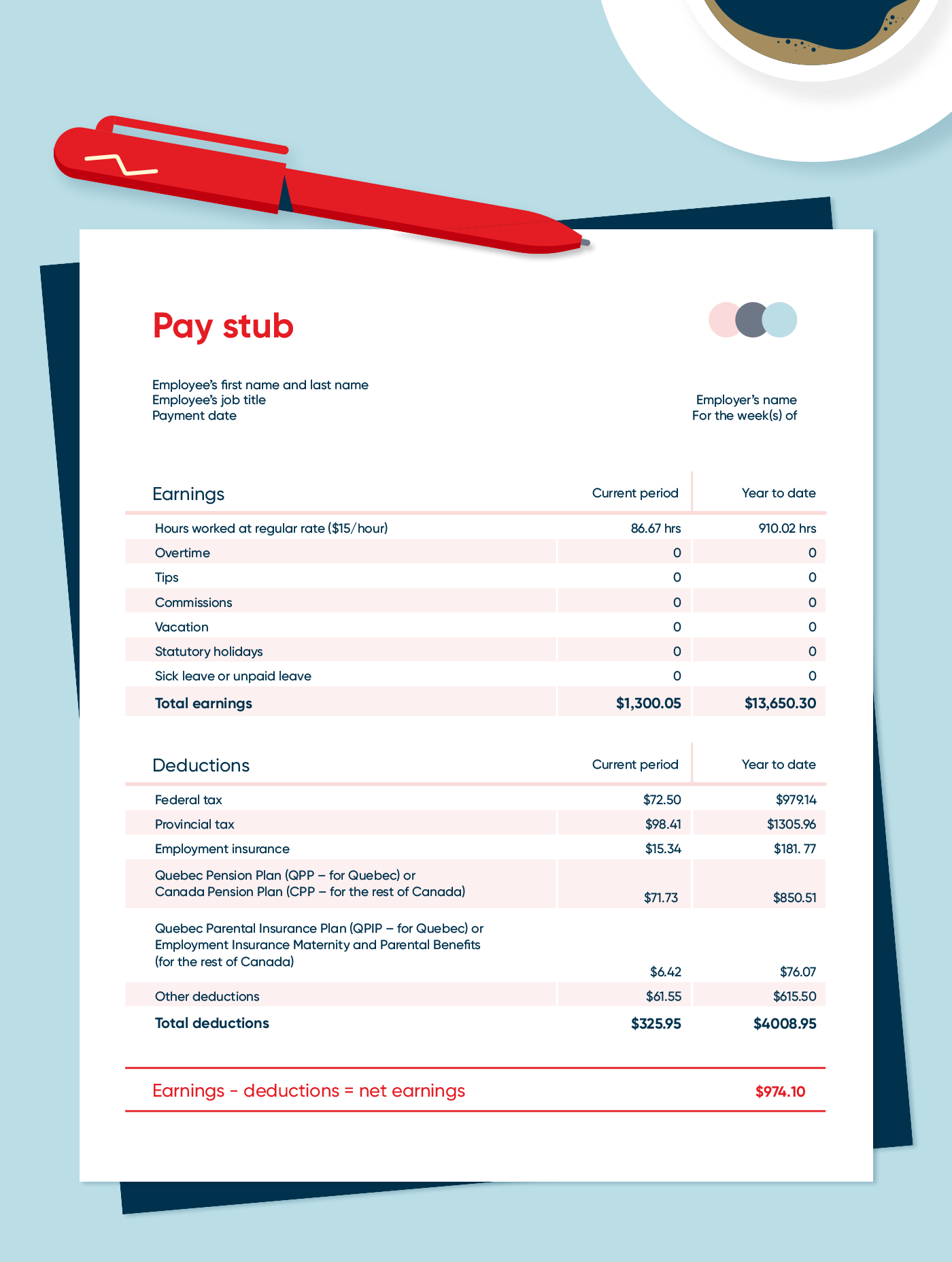

1. Identification

This section contains your identification information and that of your employer. Make sure it’s up to date. Your job title and employee number may be listed as well.

In addition, this section includes the pay period (i.e., the week[s] for which you are being paid), the payment date, and sometimes a pay period number (e.g., 12/26 for biweekly pay periods).

2. Earnings

This section shows you the number of hours you worked and your hourly rate (how much you’re paid per hour of work). Make sure this information is accurate.

It may also include overtime, which may be paid at a higher rate depending on your employer’s policy. If applicable for your job, this section will also contain tips or commissions. It also includes incentives, bonuses, and allowances. Together, these amounts make up your gross pay before deductions (e.g., income tax).

The following lines may also be included:

- Vacation pay: Either the number of hours or the amount accrued for your next vacation (typically 4% to 6% of your salary).

- Statutory holidays: Holidays for which you get paid.

- Sickness or incidental absences: If you were sick or absent on a scheduled work day.

3. Deductions

This is where abbreviations come in. This section lists all deductions at source, i.e., amounts that your employer takes from your pay and remits to the government.

As a wage earner, you must contribute to public services such as health insurance, employment insurance, road construction, schools, and more.

Here are the main deductions:

- Federal and provincial taxes: These deductions are calculated based on your gross income and a progressive tax rate. The more money you make, the more you pay in taxes. If you have two jobs or other income, don’t be surprised if you have to pay additional taxes at the end of the year.

- Employment insurance (EI): This contribution helps fund benefits for people who have lost their jobs, are on disability or maternity leave, etc. Should you lose your job, you will also be entitled to EI benefits and will be very grateful for them.

- CPP and QPP: CPP stands for Canada Pension Plan. In Quebec, workers contribute to the QPP—the Quebec Pension Plan—a government pension fund for all workers, employed and self-employed. You’ll contribute to it for as long as you’re employed. When you retire, you’ll receive a monthly pension from the plan to which you contributed.

- QPIP and EI Maternity and Parental Benefits: The Quebec Parental Insurance Plan is exclusive to Quebec. Your contributions allow new parents to take parental leave when they have or adopt a baby. The benefits cover part of their lost income. In other Canadian provinces, workers contribute to Employment Insurance Maternity and Parental Benefits. There’s no abbreviation for this program.

Other deductions on your pay stub

- Group insurance: Many employers offer group insurance to help pay for certain expenses. Coverage can include dental care, vision care, prescription drugs, disability insurance, and more. If you’re enrolled in a group insurance plan, a certain amount will be deducted from each of your paycheques.

- Group SIPP, DPSP, DBP, DCP, VRSP, or RRSP: These acronyms stand for the various types of retirement plans that your employer can offer. There are several advantages to these plans, such as helping workers save for retirement. Your employer may choose to contribute to the employee pension plan, allowing you to save even more money for your golden years. If you have access to an employer-sponsored retirement plan, you should take advantage of it.

- ESPP: An Employee Stock Purchase Plan (ESPP) is an arrangement that allows employees to purchase company stock if the company is publicly traded. Becoming a shareholder in your company can be rewarding, especially if your employer matches your contributions.

- Other deductions: Your employer may also deduct amounts for union dues, professional association fees, transfers to your individual registered savings plans, and charitable donations.

A word of advice: Errors can always happen, even with deductions. For example, if you agree with your employer to join the group insurance plan when you start working (and not after three months as is usually the case), make sure there’s a deduction on your first paycheque. Payroll may not have received the information. It’s always a good idea to check your pay stub for errors.

4. Net pay

This is the shortest section, but probably the most important one to you. This is the money you have left after all deductions have been taken from your gross pay. It’s the amount deposited in your bank account.

You will also find a summary of your year-to-date earnings and deductions in this section.

Whether you're working, studying or taking a year off

Pay no monthly fees if you're 18 to 24

How long should I keep my pay stubs?

You should keep your pay stubs in a safe place for the rest of the year. Create a folder (digital or cardboard) to file them in as you get them. Once you’ve received the last pay stub of the year, you no longer need to keep the others since the last pay stub shows the year-to-date amounts for the previous 12 months.

Be sure to dispose of the other statements securely (hello shredding!) since they contain your personal information. You don’t want them to fall into the wrong hands.

We recommend that you keep your pay stubs (at least the year-to-date ones) for 6 years after filing your tax return. This rule applies to all documents related to your tax returns. That way you’ll have everything you need in case you get audited, which will hopefully never happen.

Here’s an example of a pay stub

By now you should have a better understanding of the acronyms and deductions appearing on your pay stub, but if you’re still unsure about anything, ask your employer for clarification.

If you’re wondering what to do with the money you earn, you can develop a savings plan, make a budget (if you haven’t already), set up an emergency fund for unforeseen events, and start saving for the future.

For money management tips, subscribe to our newsletter. If you have any questions, we can answer them.